What Happened to Crypto Arbitrage in South Africa?

For a period, crypto arbitrage was one of South Africa’s most unusual financial opportunities.

The basic idea was simple: buy Bitcoin or a dollar stablecoin offshore, sell it locally at a higher rand price, and keep the difference after costs. The local premium existed because moving money, crypto, and settlement value between South Africa and offshore markets was not frictionless.

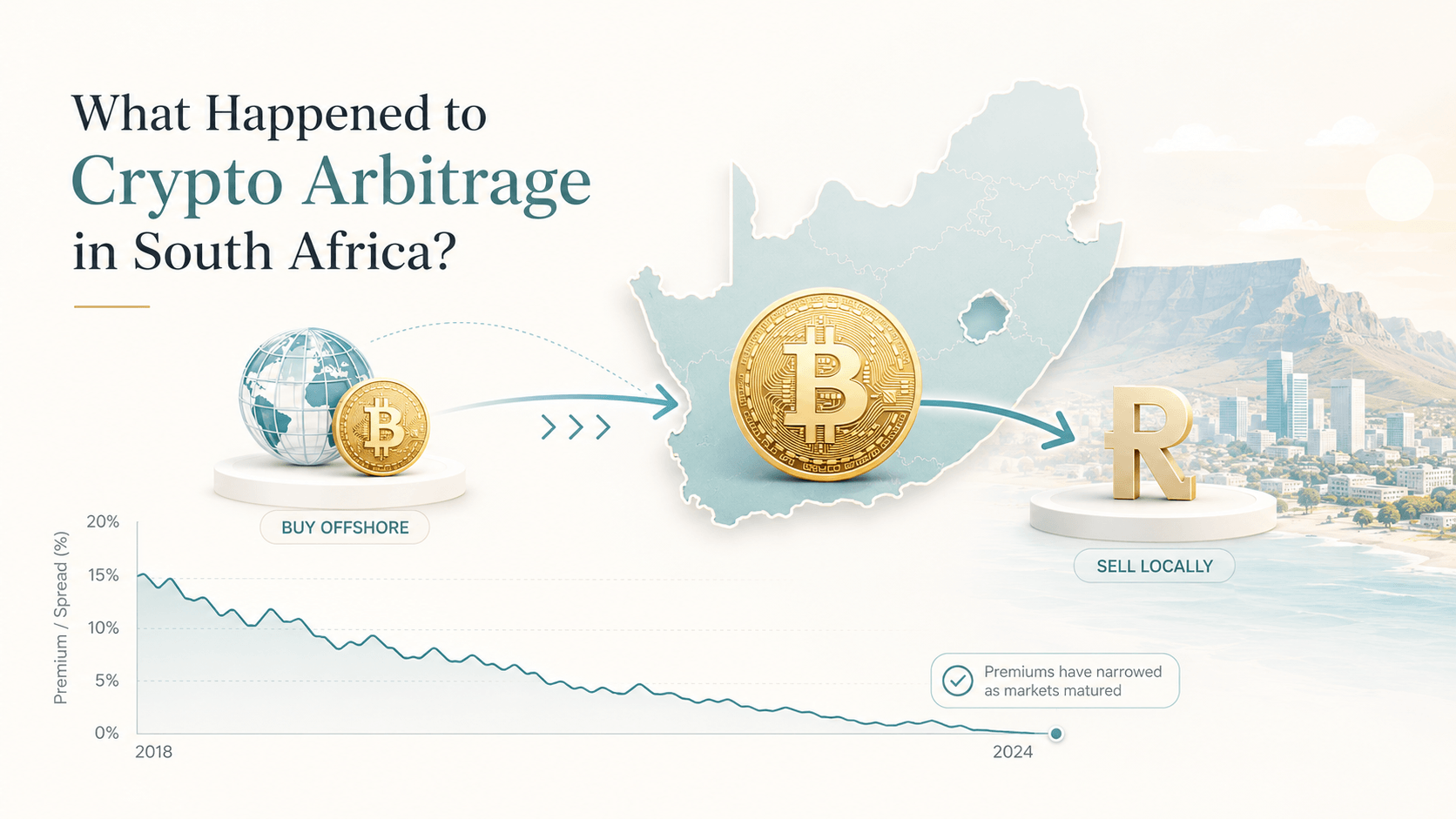

During the early boom years, the premium was often substantial. A June 2026 Moneyweb review of historical ZArbitrage data noted that premiums regularly reached 10% in 2017 and 2018, and exceeded 20% on several occasions. Even after that peak, same-day spreads of 4% to 5% were possible for a time.

That opportunity attracted thousands of South Africans and eventually became a proper fintech niche. Firms built exchange integrations, foreign-exchange workflows, client dashboards, hedging systems, compliance processes, and settlement infrastructure around it.

But the opportunity changed.

By 2023, the spread had narrowed to about 2%. By January 2026 it was around 1% before costs, with occasional short-lived increases. In early June 2026, the average premium was reported as slightly below 1%. That is the central answer to what happened to arbitrage in South Africa: the premium became smaller, while the cost and complexity of capturing it became greater.

The premium was real, but it was never magic

Crypto arbitrage was not a prediction that Bitcoin would rise.

It was a market-structure trade. The same asset could trade at different prices in different places because capital controls, banking delays, foreign-exchange administration, settlement risk, liquidity constraints, and local demand created frictions between the South African and offshore markets.

Each successful arbitrage cycle helped reduce that gap. More firms buying offshore and selling locally meant more supply in the expensive market. Better software, institutional liquidity, and professional execution made the market more efficient. Eventually, the premium that attracted the industry was compressed by the industry itself.

A 1% gross spread is very different from a 10% or 20% spread. At that level, bank fees, foreign-exchange margins, trading charges, settlement delays, tax, service fees, and operational errors can consume most or all of the expected profit.

The question stopped being “Can I see a premium?” and became “Can I execute the entire cycle cheaply, compliantly, and reliably?”

The difficult part was always the financial plumbing

A crypto arbitrage transaction involved much more than two exchange accounts.

- Use a client’s own capital and available foreign-exchange allowance.

- Convert rands into foreign currency through a compliant channel.

- Purchase crypto or stablecoins offshore.

- Sell the asset in South Africa at the local premium.

- Settle the rand proceeds and retain the spread after all costs.

The South African Reserve Bank’s Financial Surveillance FAQ illustrates why this is sensitive. It says individuals may purchase crypto assets abroad using the applicable single discretionary allowance and foreign capital allowance, subject to the relevant requirements. It also states that people may not use another person’s allowance through a loan or similar arrangement.

That is why credible arbitrage businesses were never simply “crypto platforms”. They were combinations of financial-services providers, foreign-exchange intermediaries, banks, exchanges, OTC desks, compliance systems, and technology.

Fynbos Finance shows what the modern model looks like

Fynbos Finance is useful because it makes the multi-party nature of arbitrage visible. Its public material describes a crypto-arbitrage service built around offshore purchase and local sale, with regulatory and operational infrastructure around the trade.

The foreign-exchange leg is particularly important. The Fynbos Arbitrage page says Fynbos has partnered with Kuda FX, a registered Financial Services Provider, for the forex component. Kuda’s own arbitrage page says it has partnered with Fynbos Arbitrage and describes Fynbos Arbitrage as a licensed crypto-asset service provider regulated by the Financial Sector Conduct Authority.

That matters because the trade does not work without the foreign-exchange leg. The crypto asset may be bought and sold quickly, but the rand-to-foreign-currency transfer, offshore remittance, source-of-funds checks, settlement, and compliance recordkeeping are where much of the operational work happens.

Banking and settlement infrastructure changed the market

The market’s early weakness was its dependence on banks and payment routes that were often uncomfortable with crypto-related activity.

In November 2019, FNB announced that it would withdraw services from cryptocurrency platforms, including Luno, effective 31 March 2020. Luno published a statement on the proposed FNB account closure, and MyBroadband reported that several South African crypto-linked bank accounts were affected.

These were historical de-risking decisions and should not be read as descriptions of any bank’s current policy. The point is narrower: a profitable-looking arbitrage spread is worthless if the banking rail required to complete the cycle stops working.

The same theme appeared again in 2023. A Moneyweb article marked as sponsored by Currency Hub said a payment-route disruption had affected arbitrage providers that relied on it. Currency Hub said it was unaffected because it had an alternative fiat-to-crypto on-ramp. That account should be read as the company’s own description of the event, not as an independent regulatory finding.

Still, the broader lesson is sound. Arbitrage was never only about pricing. It was about access to reliable payment rails.

Currency Hub and Koinexpert: consolidation, not disappearance

Currency Hub became part of the story because it represented the infrastructure-heavy end of the market. Its website describes the business as a South African regulated financial-services provider offering institutional foreign exchange, crypto arbitrage trading, OTC desk services, and related financial services.

The FSCA has also published lists and updates relating to authorised crypto-asset service providers. Public FSCA records identify Black Onyx Currency Hub (Pty) Ltd under FSP number 50850, with authorised activities including advice, intermediary services, and investment management.

In May 2023, Currency Hub announced that it would take over arbitrage trading for Koinexpert clients. The announcement appeared in the sponsored Moneyweb article mentioned above, which said the transition followed growing licensing and operational demands on providers.

Koinexpert’s own domain now routes users toward Currency Hub. A Teruza case study on the Koinexpert platform describes it as a trading engine used to execute more than R3 billion in arbitrage trades over roughly 2.5 years. Teruza also notes Koinexpert-related experience on its fintech services page. These figures are company-reported, but they capture an important part of the market’s legacy: expertise developed in crypto arbitrage could be redeployed into mainstream fintech, automation, and trading infrastructure.

The important story is not that one company stopped offering a retail arbitrage service. It is that the sector began consolidating around providers with deeper compliance, foreign-exchange, and settlement capability.

Shiftly shows what shrinking margins look like

Shiftly illustrates the later stage of the market.

The company launched publicly in 2019 and described its founders as having arbitraged in a personal capacity since 2014. Its website published performance information and warned that past performance did not guarantee future results.

The Shiftly performance page now states that its arbitrage service closed on 31 October 2025.

The closure notice does not, by itself, establish why the service ended. It should not be treated as evidence of misconduct. But it fits the wider commercial pattern: when spreads narrow, a provider must generate more volume and operate with lower costs simply to earn the same return.

OVEX made a similar strategic decision earlier. Moneyweb reported that OVEX would close its crypto-arbitrage service on 31 January 2022 while continuing other crypto-business lines. VALR also announced in 2022 that it would stop offering crypto arbitrage to new customers and wind down the service for existing customers.

This is what a maturing market often looks like. Some firms scale. Some consolidate. Some move into adjacent services. Some close a product that no longer justifies the operational burden.

Regulation is still moving

South Africa’s crypto-arbitrage industry matured at the same time that crypto regulation became more formal.

In October 2022, crypto assets were declared financial products under South Africa’s financial-advice framework. The FSCA subsequently began licensing crypto-asset service providers under the FAIS Act. A 2026 FSCA update on licensing and supervision of crypto-asset service providers described the continuing licensing process.

The next major change may be the proposed Capital Flow Management Regulations. The South African Reserve Bank announced in April 2026 that National Treasury had published the draft Capital Flow Management Regulations of 2026 for public comment. The Parliamentary Monitoring Group summary says one objective is to bring crypto assets within the exchange-control framework to address risks and ensure oversight of emerging financial instruments.

The draft regulations were still proposals in the official material reviewed for this article. Their final form, transition rules, thresholds, and associated crypto-asset manual will matter greatly to businesses that move value across borders.

So, is crypto arbitrage dead?

No. But the old version is.

South Africa still has local and offshore price differences. The premium can widen temporarily when the rand moves, demand changes, or market liquidity becomes uneven. But the large and repeatable spreads of the early years have been replaced by thin, competitive margins.

The practical summary

- The premium was real, but it was created by market friction.

- Professional arbitrage reduced the very spread it exploited.

- Regulation, banking access, foreign exchange, and settlement infrastructure became decisive.

- Fynbos Finance and Currency Hub show the more specialised provider model.

- Koinexpert shows how arbitrage infrastructure became broader fintech capability.

- Shiftly shows how retail-facing arbitrage services can close when margins shrink.

For firms such as Fynbos Finance and Currency Hub, the opportunity is no longer simply finding a premium. It is executing a compliant transaction stack involving forex, banks, exchanges, OTC liquidity, hedging, settlement, and client administration.

For Koinexpert, the story is that a substantial arbitrage platform became part of a broader fintech capability base.

For Shiftly, the story is that a well-known retail service could close when the margin and operating environment changed.

Crypto arbitrage in South Africa did not vanish. It became more efficient, more regulated, more infrastructure-dependent, and far less forgiving.

That is what happened to arbitrage.

Sources and further reading

- Moneyweb: Crypto arbitrage premium hits “new normal” below 1%

- Moneyweb: What’s happened to the crypto arbitrage spread?

- Moneyweb: Why crypto arbitrage is interesting again

- Fynbos Finance

- Fynbos Finance: Fynbos Arbitrage

- Kuda FX: Digital asset arbitrage partnership with Fynbos Arbitrage

- Currency Hub

- Koinexpert

- Teruza: Koinexpert case study

- Teruza: Fintech services and Koinexpert platform reference

- Shiftly

- Shiftly: Performance and arbitrage-service closure notice

- Moneyweb: OVEX exits crypto arbitrage

- Moneyweb: VALR exits new crypto-arbitrage business

- Luno: Statement on proposed FNB bank-account closure

- MyBroadband: FNB shuts down South African cryptocurrency-linked bank accounts

- South African Reserve Bank: Financial Surveillance FAQ

- Financial Sector Conduct Authority

- FSCA: Update on licensing and supervision of crypto-asset service providers

- SARB: Draft Capital Flow Management Regulations open for public comment

- National Treasury: Draft Capital Flow Management Regulations 2026

- PMG: Draft Capital Flow Management Regulations 2026